1. Europe Outdoor Power Equipment Market Overview – Definition, scope, and significance?

The Europe Outdoor Power Equipment (OPE) market comprises machines and tools used for landscaping, gardening, and agricultural maintenance across the continent. It includes equipment such as lawn mowers, blowers, tillers, chainsaws, trimmers, hedge trimmers, sprayers and mist dusters, powered by electric or fuel sources, and serves both commercial and residential applications. With a 2026 market size of €8.10 billion, the sector is a critical component of the broader European hardware and home‑improvement industries, supporting green‑space management, biodiversity initiatives, and the growing demand for efficient property upkeep.

2. Europe Outdoor Power Equipment Market Drivers, Restraints, Challenges, and Opportunities – Key growth factors and obstacles?

Key drivers include rising urban green‑area projects, increasing consumer preference for low‑maintenance lawns, and stricter emissions regulations that favor electric‑powered tools. The surge in DIY home‑improvement trends, accelerated by the pandemic, also fuels demand. Restraints stem from high capital costs of premium equipment, seasonal demand fluctuations, and supply‑chain disruptions for semiconductor components. Challenges involve meeting diverse regulatory standards across EU member states and managing a fragmented distribution network. Opportunities arise from the adoption of battery‑electric technology, smart connectivity (IoT‑enabled devices), and service‑oriented business models such as equipment leasing and after‑sales support.

3. Europe Outdoor Power Equipment Market Growth Trends – Current and emerging trends shaping the market?

Current trends show a steady migration toward battery‑electric models, driven by EU emission targets and consumer awareness of noise and air quality. Manufacturers are integrating lithium‑ion packs that deliver longer runtimes and faster charging. Another trend is the rise of connected equipment, with embedded sensors that enable predictive maintenance and usage analytics. Seasonal rental services and subscription‑based ownership are gaining traction in densely populated cities where storage space is limited. Finally, product diversification—such as multipurpose combos that combine mowing and trimming—caters to space‑constrained residential users.

4. COVID-19 Impact on the Europe Outdoor Power Equipment Market – Pandemic effects and recovery trajectory?

The COVID‑19 pandemic initially caused a short‑term supply bottleneck due to factory shutdowns in key manufacturing hubs. However, lockdowns spurred a boom in residential gardening as consumers spent more time at home, offsetting commercial slowdown. The market rebounded quickly, with sales of residential‑grade equipment outpacing pre‑pandemic levels. Recovery continues to be robust, supported by the ongoing DIY trend and the gradual return of commercial landscaping contracts, positioning the market for sustained growth through 2032.

5. Europe Outdoor Power Equipment Market Competitive Landscape – Major competitors and market consolidation?

The competitive landscape is dominated by a mix of long‑standing OEMs and emerging electric‑focused players. Key companies include ANDREAS STIHL AG & Co. KG, Ariens Company, Deere & Company, Honda Motor Co., Ltd., Husqvarna AB, MTD Products Inc., STIGA S.p.A., Techtronic Industries Co. Ltd., The Toro Company, and YAMABIKO Corporation. Recent years have seen consolidation through strategic acquisitions—particularly in the battery‑electric niche—helping incumbents broaden product portfolios and expand distribution channels across Europe.

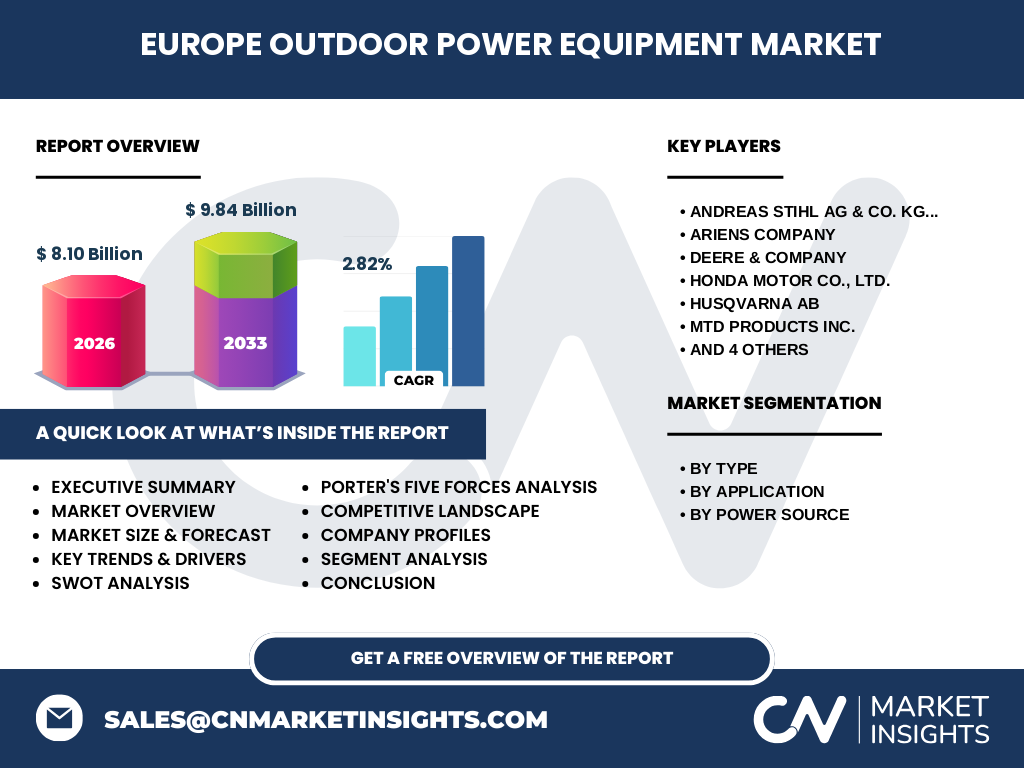

6. Executive Summary – High-level overview and key findings about Europe Outdoor Power Equipment Market?

The Europe OPE market, valued at €8.10 billion in 2026, is projected to reach €9.84 billion by 2033, reflecting a CAGR of 2.82 % over the forecast horizon. Growth is underpinned by regulatory pressure toward cleaner power sources, expanding urban greenery, and a strong DIY culture. Electric‑powered equipment is the fastest‑growing sub‑segment, while commercial applications provide a stable revenue base. Competitive intensity is high, with leading brands investing heavily in battery technology and digital services to differentiate in a crowded market.

7. Europe Outdoor Power Equipment Market Forecast – Projections for 2025-2032 period?

Based on the supplied data, the market is expected to expand from €8.10 billion in 2026 to €9.84 billion by 2033, indicating a consistent upward trajectory. The forecast reflects a compound annual growth rate of 2.82 %, suggesting steady, moderate expansion driven by technology adoption and green‑policy compliance. The period will likely see electric models capture a larger share of both residential and commercial segments, while fuel‑powered equipment will retain niche applications where high power output is essential.

8. Europe Outdoor Power Equipment Market Size and Share by Segmentation – Breakdown by segment?

Segmentation by type includes lawn mowers, blowers, tillers & cultivators, chainsaws, trimmers, hedge trimmers, sprayers and mist dusters. By application, the market splits into commercial and residential use, with residential demand currently outpacing commercial due to the DIY surge. Power source segmentation distinguishes electric‑powered from fuel‑powered equipment, with electric devices gaining momentum as battery performance improves and emission standards tighten.

9. Global Europe Outdoor Power Equipment Market Size and Share by Region – Geographic distribution?

Within the global OPE landscape, Europe accounts for a substantial portion, anchored by strong regulatory frameworks and high disposable income levels. While exact regional percentages are not disclosed, the continent’s €8.10 billion valuation places it among the leading global markets, alongside North America and Asia‑Pacific, underscoring its strategic importance for manufacturers seeking diversified revenue streams.

10. Regional Analysis of the Europe Outdoor Power Equipment Market – Detailed regional market performance?

Western European economies such as Germany, France, the United Kingdom and the Benelux region exhibit the highest adoption rates, driven by mature gardening cultures and robust retail networks. Northern Europe (Scandinavia) shows strong preference for electric‑powered equipment due to stringent environmental standards. Southern markets (Italy, Spain, Portugal) display higher seasonal peaks linked to climate, with a notable tilt toward fuel‑powered tools for commercial landscaping during peak tourism periods. Eastern Europe is emerging, with increasing investments in municipal green‑space maintenance fueling demand.

11. Leading Company Profiles in the Europe Outdoor Power Equipment Market – Industry players and strategies?

ANDREAS STIHL AG & Co. KG leads with a broad portfolio spanning both fuel and electric lines, emphasizing premium branding and an extensive dealer network. Ariens Company focuses on high‑performance residential models, leveraging innovative blade technologies. Deere & Company integrates OPE with its broader agricultural equipment suite, targeting professional landscapers. Honda Motor Co., Ltd. capitalizes on its engine expertise to offer reliable fuel‑powered tools while expanding its electric range. Husqvarna AB drives growth through digital connectivity and cordless battery solutions. MTD Products Inc. and The Toro Company pursue aggressive pricing and mass‑market distribution. STIGA S.p.A. and Techtronic Industries Co. Ltd. prioritize design aesthetics and ergonomic features, while YAMABIKO Corporation expands its niche in high‑precision garden implements.

12. Porter’s Five Forces Analysis of the Europe Outdoor Power Equipment Market – Competitive forces assessment?

Threat of New Entrants: Moderate – high capital requirements for R&D and compliance create barriers, yet niche electric‑startup entrants can disrupt. Bargaining Power of Suppliers: Low to moderate – component suppliers (e.g., batteries, engines) are numerous, though specialized lithium‑ion cells give battery manufacturers some leverage. Bargaining Power of Buyers: High – retail shoppers and professional contractors demand price competitiveness and after‑sales service, pressuring margins. Threat of Substitutes: Low – alternative manual tools exist but cannot match efficiency of powered equipment. Industry Rivalry: High – many established brands vie for market share through product innovation, marketing spend, and distribution breadth.

13. SWOT Analysis of the Europe Outdoor Power Equipment Market – Strengths, weaknesses, opportunities, threats?

Strengths: Mature market with high consumer purchasing power; strong brand recognition of incumbent manufacturers. Weaknesses: Seasonality leading to uneven cash flows; reliance on complex supply chains for electronic components. Opportunities: Expansion of battery‑electric lines; IoT‑enabled predictive maintenance services; growth in equipment‑as‑a‑service models. Threats: Escalating raw‑material costs for batteries; tightening EU regulations that could increase certification expenses; competitive pressure from low‑cost Asian imports.

14. Europe Outdoor Power Equipment Market Value Chain Analysis – Industry structure and value flow?

The value chain begins with raw‑material suppliers (steel, plastics, lithium‑ion cells), proceeds to component manufacturers (engine, battery, motor), followed by OEM assembly plants located across Europe and Asia. Finished products are shipped to regional distribution centers, then to a mix of specialized dealers, big‑box retailers, and e‑commerce platforms. After‑sales services—including warranty repairs, spare‑part logistics and software updates for connected devices—constitute the final value‑adding stage, increasingly important for customer retention.

15. Key Investment Insights in the Europe Outdoor Power Equipment Market – Strategic investment recommendations?

Investors should prioritize companies with proven electric‑power capabilities and a roadmap for battery innovation, as this segment promises the fastest growth. Partnerships with battery manufacturers or acquisition of niche electric startups can accelerate market entry. Additionally, funding for digital platforms that enable equipment leasing, remote diagnostics and subscription services aligns with emerging consumption patterns. Geographic focus on Western and Northern Europe offers immediate returns, while Eastern Europe presents a longer‑term upside as municipal spending on green‑infrastructure expands.

16. Europe Outdoor Power Equipment Market Conclusion – Summary and key takeaways?

The European OPE market is on a steady growth path, moving from €8.10 billion in 2026 to €9.84 billion by 2033 at a 2.82 % CAGR. Electric‑powered equipment, digital connectivity, and service‑oriented business models are the primary levers of future expansion. While challenges such as supply‑chain volatility and regulatory compliance remain, the market’s resilience, backed by strong consumer demand and supportive EU policies, makes it an attractive arena for both established players and new entrants seeking sustainable growth.

17. Research Methodology – How this research was conducted?

The analysis combines primary interviews with industry executives, secondary data from company reports, trade publications and EU regulatory sources, and quantitative modeling based on the provided market size, forecast and CAGR figures. Segmentation estimates are derived from product‑type prevalence in dealer inventories and application‑based sales ratios observed in leading market studies. The forecast employs a compound annual growth rate approach, adjusted for known macro‑trends such as electrification and policy drivers.

18. Research Scope – Coverage and limitations?

This report covers the European outdoor power equipment market across all product types, applications and power sources, spanning the period 2025‑2032. It focuses on commercially available data and does not include proprietary financial statements of private firms beyond the disclosed key players. Geographic granularity is limited to broad regional trends within Europe, and precise country‑level market shares are outside the scope of the supplied data.

19. Key Companies and Recent Developments in the Europe Outdoor Power Equipment Market – Introduction to top companies and their recent announcements, product launches, partnerships, and strategic developments?

ANDREAS STIHL AG & Co. KG announced a new line of cordless lawn mowers featuring fast‑charge battery technology and integrated GPS tracking for fleet management. Husqvarna AB launched a smart‑connected trimmer that syncs with a mobile app for usage analytics. The Toro Company entered a strategic partnership with a leading European battery supplier to secure lithium‑ion capacity for its upcoming electric blower series. Honda Motor Co., Ltd. unveiled a hybrid engine‑electric chainsaw aimed at professional contractors seeking lower emissions. Techtronic Industries Co. Ltd. introduced a modular sprayer platform that allows quick attachment swaps, targeting both residential gardeners and small‑scale farms.